One option is to just sell the house to settle the home mortgage, and distribute any remaining funds from the sale to the successors as determined by the will or the laws in your state. If you wish to retain the house, you'll need to work with the servicer to get the home loan transferred to you.

If there was a reverse mortgage on the residential or commercial property, the loan quantity becomes due after the death of the borrower. If the heir to the house wishes to maintain the home, they'll need to repay the loan. Otherwise, they can sell the house or turn the deed over to the reverse mortgage servicer to please the debt.

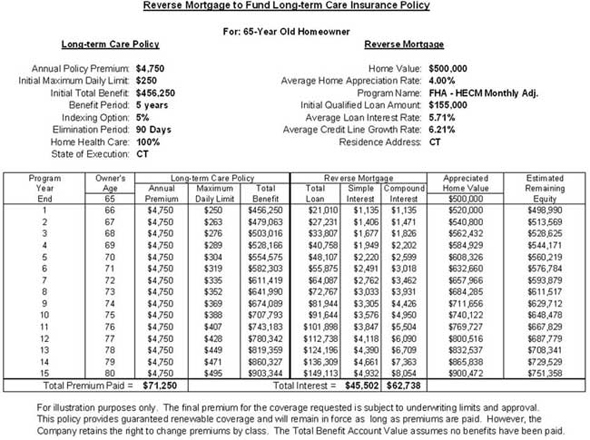

The reverse home mortgage is a popular approach used by older house owners to make the most of equity in their houses. Open to house owners 62 or older, the reverse home loan can offer them constant home equity income. Additionally, the older a house owner is, the more equity income a reverse mortgage provides in return (what act loaned money to refinance mortgages).

Reverse home mortgages are available to homeowners fulfilling age requirements and who totally own or have significant equity in their houses. The home secures a homeowner's reverse home mortgage. While no payments are made by a house owner with a reverse home mortgage, the home mortgage is due upon death. Estate assets can pay back a reverse home mortgage.

Reverse home mortgages are repaid in numerous various methods. In addition to the estate of the deceased, beneficiaries to the reverse mortgaged house can also repay the loan in full. Reverse home mortgage lenders often offer beneficiaries from 3 to 12 months to pay back the loan. If neither the beneficiaries nor the estate pay back the loan, the loan provider usually reclaims the house.

As lienholders, lending institutions can look for foreclosure on the houses protecting their loans when they're not paid back. In cases in which a reverse home loan lender winds up foreclosing, it will try to sell the house to satisfy its loan. Any profits left over after a reverse mortgage lending institution forecloses and offers a home usually go to the departed borrower's beneficiaries or estate.

Some Ideas on How To Switch Mortgages While Being You Need To Know

By law, reverse home mortgages are non-recourse loans, suggesting lending institutions can't pursue property owner estates or heirs for any mortgage deficiencies staying after sale (how to compare mortgages excel with pmi and taxes). Thankfully, lots of reverse mortgages fall under the Federal Real estate Administration's Home Equity Conversion Home mortgage program. All FHA-based reverse home mortgages include special home loan insurance coverage to cover their lending institutions must mortgage shortages result when successors offer those homes.

Much like a conventional mortgage, there are expenses connected with getting a reverse home loan, specifically the House Equity Conversion Mortgage (HECM). These costs are usually greater than those related to a standard mortgage. Here are a few costs you can expect. The in advance home loan insurance coverage premium (MIP) is paid to the FHA when you close your loan.

If the home offers for less than what is due on the loan, this insurance coverage covers the distinction so you won't wind up underwater on your loan and the lender doesn't lose money on their financial investment. It also secures you from losing your loan if your lender fails or can no https://expressdigest.com/timeshare-fraudster-62-is-told-to-pay-back-20000/ longer meet its responsibilities for whatever reason.

The expense of the in advance MIP is 2% of the assessed value of the house or $726,535 (the FHA's loaning limitation), whichever is less. For instance, if you own a house that's worth $250,000, your in advance MIP will cost around $5,000. In addition to an in advance MIP, there is also an annual MIP that accumulates every year and is paid when the loan comes due.

5% of the loan balance. The home mortgage origination cost is the quantity of cash a lender charges to stem and process your loan. This cost is 2% of the first $200,000 of the home's worth plus 1% of the remaining worth after that. The FHA has actually set a minimum and optimum expense of the origination fee, so no matter what your house is valued, you will not pay less than $2,500 or more than $6,000.

The maintenance fee is a regular monthly charge by the lender to service and administer the loan and can cost approximately $35 every month. Appraisals are required by HUD and figure out the marketplace worth of your home. While the real expense of your appraisal will depend upon factors like place and size of the house, they typically cost in between $300 and $500.

Not known Details About What Does It Mean When People Say They Have Muliple Mortgages On A House

These costs may consist of: Credit report charges: $30 $50 File preparation charges: $50 $100 Courier https://geekinsider.com/the-problem-with-timeshares-and-how-primeshare-differentiates/ fees: $50 Escrow, or closing fee: $150 $800 Title insurance coverage: Depend upon your loan and location There are lots of aspects that influence the interest rate for a reverse home loan, including the lending institution you work with, the kind of loan you get and whether you get a repaired- or adjustable rate mortgage (how common are principal only additional payments mortgages).

A reverse home mortgage is a way for eligible homeowners to take advantage of the equity in their homes to satisfy retirement expenditures. To certify, you need to be age sixty-two (62) or over, occupy the property as your main house, and own the house outright or have enough equity in the house.

The loan accumulates interest and other fees that are not due up until a trigger event takes place. However, the borrower is still accountable for real estate tax, house owner insurance coverage, house owner association fees (if any), and maintenance. There are three options for loan profits to be distributed to the customer: a lump amount, a month-to-month payment amount, or a home equity line of credit.

The borrower no longer utilizes the home as a primary home for more than 12 successive months. (A debtor can be far from the house, e. g., in an assisted living home, for up to 12 months due to physical or mental disorder. If the move is permanent the loan ends up being due).

If an enduring spouse is not also a debtor, likely due to the fact that she/he is under age 62, https://www.thewowstyle.com/is-a-timeshare-really-cheaper-than-a-hotel-when-going-on-vacation/ a federal case, cited in Oregon cases, holds that the loan provider can not foreclose against a making it through spouse non-borrower at the death of the spouse/borrower. Nevertheless, the loan is still due as discussed above. If a home with a reverse home loan becomes based on probate, the home loan is still an encumbrance on the home.